The Truth About Portfolio Rebalancing

Feb 25, 2025

Since 2001, I’ve worked with clients and advisors, and I’ve seen countless examples of what I call “teeter-totter portfolios.” These are portfolios where growth goes up, then down, but the growth never seems to stick around for long. It vanishes as if it were written in some disappearing ink. So what’s going on here? This question led me to experiment with my own account to uncover the answer, which I’ll get to in a moment.

ASSET ALLOCATION = RECIPE

To understand portfolio rebalancing, we first need to understand asset allocation. Asset allocation is simply a strategy, a recipe of investments based on your risk tolerance, time horizon, and investment knowledge. Everyone’s investment mix is unique.

Let’s use a cookie recipe analogy to explain. Ingredients like flour, sugar, eggs, chocolate chips, and vanilla need to be balanced. Too much of any ingredient and the cookies will be soggy; too little, and they’ll be hard and clumpy. Investing works the same way. The choices you make in your portfolio will affect returns and risk.

If you’ve ever baked cookies, you didn’t just throw dough on a tray and hope for the best, right? You probably checked the cookies along the way—much like portfolio rebalancing.

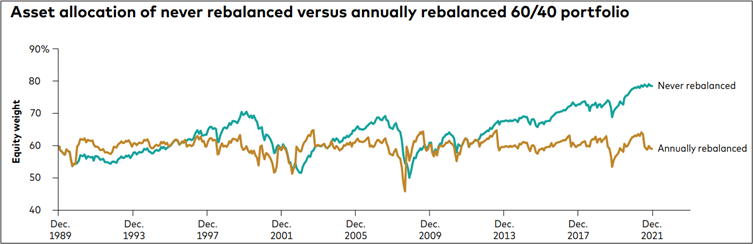

But does it work? Does it lead to better returns? Well, let’s look at some hard data. In 2007, Vanguard, one of the largest investment management firms, did a 40-year study. They found that rebalancing a portfolio can reduce returns by up to 2.037%. To put that into perspective, on a $100,000 portfolio over 25 years, a 2.037% loss could result in $165,000 less in returns.

It’s interesting that Vanguard, a company that offers portfolio rebalancing, found that it can diminish returns. A separate study by Sigma Research, over a 30-year period, showed that portfolios without rebalancing actually outperformed rebalanced ones. So what’s going on?

Back in 2001, portfolio rebalancing was a big trend. Every fund company touted it as a value-add. But if it’s their job to balance portfolios, why does it seem to hurt returns? The answer is simple: rebalancing keeps us invested. It smooths out the highs and lows, which keeps us from pulling out when the market dips.

Fund companies, insurance firms, and large corporations know consumer behaviour well. They know that if our portfolios become too volatile, we’ll abandon ship. So they use rebalancing as a tool to keep us in the ride, smoothing out the roller coaster effect so we don’t panic and sell. It’s like ballast in a ship—it keeps us steady so we don’t make emotional decisions that might hurt long-term growth. This is exactly why portfolio rebalancing exists. It wasn’t designed to boost returns; it’s meant to keep us in the game for the benefit of the fund managers and companies.

TEETER-TOTTER RETURNS

I’ve seen this in my own portfolios—growth up, growth down, never really sticking. How could I keep that 20% growth in my portfolio and make it last? That’s when I came up with “growth harvesting,” a proactive strategy that requires constant attention. Whether you're a DIY investor or have an advisor, it’s essential to stay active and not passive in your approach.

Growth harvesting involves taking some of the growth when the market is high and setting it aside for future opportunities. It’s about being proactive and reinvesting at the right time, rather than letting gains disappear into thin air. This approach has worked for me, and I use it with all my clients.

To summarise, here are the key points:

- Portfolio rebalancing manages emotions, keeping us invested even during market dips. This is why it’s valuable.

- However, it can increase risk by requiring higher equity exposure if returns fall short.

- You may not need rebalancing at all. If you can manage your portfolio proactively using growth harvesting, you can achieve better results.

If you’re working with an advisor, this approach should be part of your plan from the start, with predetermined strategies for entering and exiting the market. But remember, nobody can predict the future or time the market, so always seek sound advice from financial professionals.